Jun 26, 2026Market Insights

Spain’s Pet Parents in 2026: High Ownership, Stable Budgets, and Strong Loyalty to In‑Store Shopping

New 2026 data shows that 54% of Spanish households now have a pet, with dogs leading and mixed feeding becoming increasingly common.

New 2026 data from the Spanish Pet Industry Association (AEDPAC) reveals a pet‑loving nation defined by high ownership rates, controlled but steady spending, and a strong preference for physical retail. Dogs remain the dominant companion animal, while omnichannel habits and rising insurance adoption signal a more mature, structured pet market.

The findings are based on 713 online interviews conducted between 27 January and 9 February 2026.

1. Pet Ownership: Adoption Culture and Shifting Household Patterns

In 2026, 54% of Spanish households have at least one pet—an increase of 2 percentage points YoY.

Where Pets Come From

- 66% adopted from shelters or private individuals

- 10% taken in as strays

- 15.7% purchased from stores

Spain continues to be one of Europe’s strongest adoption‑driven markets.

Species Distribution

- Dogs appear in 3 out of 4 pet‑owning households

- Cats appear in just over half

Ownership patterns are evolving:

- Dog‑only households declined to 48.2%

- Cat‑only households remain stable at 24.5%

2. Feeding Habits: Dry Food Dominates, but Mixed Diets Grow

Dogs

- 55% rely exclusively on dry food

- 37% mix dry + wet

- 8% use wet food only

Cats

- 59.5% use mixed feeding

- 29% dry only

- 11.7% wet only

Spending on Food

Pet food represents 38.8% of monthly pet spending:

- Dog owners: €63 ($68)

- Cat owners: €53 ($57)

Both groups reduced spending by €3 compared to 2025—a “controlled adjustment” without compromising care.

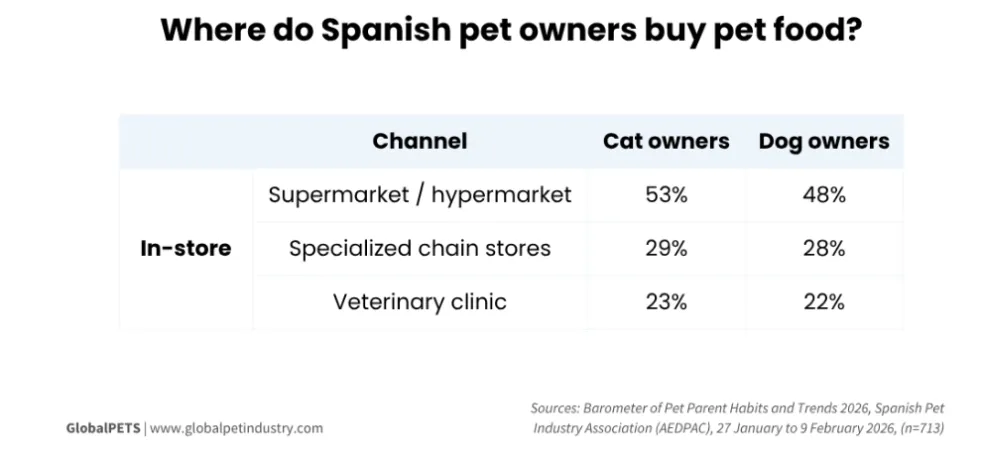

3. Offline Retail Remains the Preferred Channel

Spain stands out as one of Europe’s strongest in‑store pet food markets.

Dog Owners

- 86% buy mostly in‑store

- Supermarkets: 48%

- Specialized chains: 28%

- Veterinary clinics: 22%

Cat Owners

- 86.8% buy mostly in‑store

- Supermarkets: 53%

- Specialized chains: 22%

- Veterinary clinics: 23%

Physical retail remains dominant due to convenience, trust, and habit.

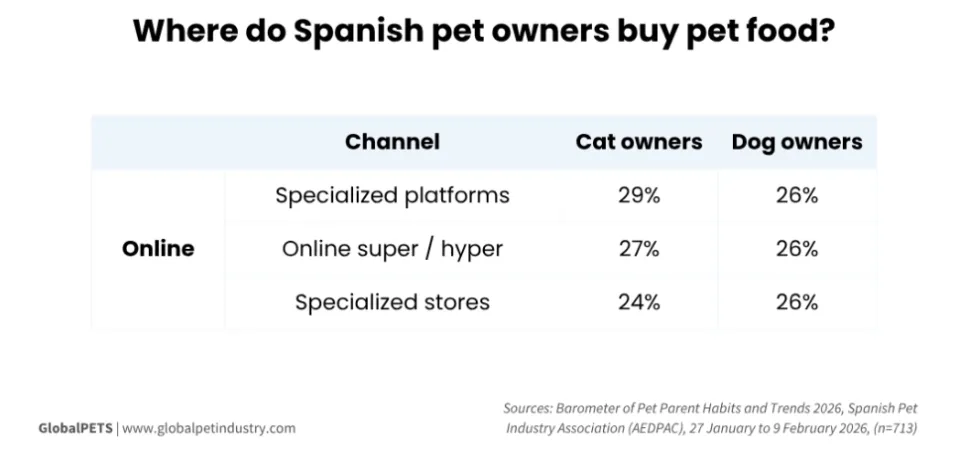

4. Online & Omnichannel: Small but Growing

Online‑only purchasing remains extremely low:

- 1% of dog owners

- <1% of cat owners

Among those who do shop online, purchasing is evenly distributed across:

- Specialized platforms

- Online supermarkets/hypermarkets

- Specialist retailers

AEDPAC highlights that 9 in 10 pet parents now combine channels, confirming omnichannel as the new standard.

“Consumers compare, switch and choose based on convenience. The hybrid experience is no longer a trend – it is the new normal.”

5. Services: Health Leads, Grooming Follows, Daycare Lags

Veterinary Care

- Over 90% of dog and cat owners** report regular vet visits

Grooming

- ~70% of dogs receive grooming/washing services

- ~50% of cats receive grooming

Daycare & Boarding

Usage remains low:

- 68.5% of dog owners do not use daycare

- 73% of cat owners do not use daycare

Spain’s service market remains health‑centric rather than lifestyle‑centric.

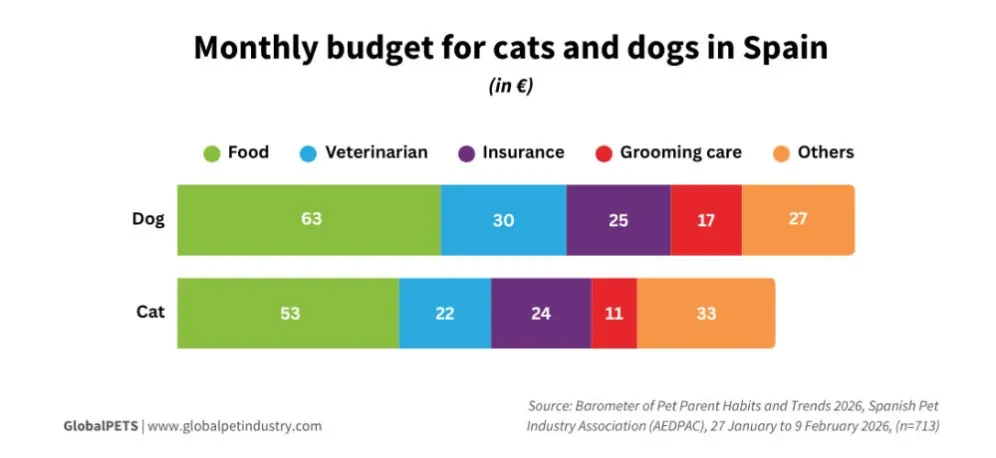

6. Monthly Budget: Controlled Spending With Rising Insurance Adoption

Average Monthly Spending

- Dogs: €163 ($176)

- Cats: €144 ($155)

Breakdown

- Food: largest share

- Veterinary care:

- Dogs: 19% (€30)

- Cats: 15% (€22)

- Grooming:

- Dogs: 11% (€17)

- Cats: 8% (€11)

- Other expenses (hygiene, toys, accessories, gifts):

- Dogs: €27

- Cats: €33

Insurance

Insurance adoption is rising:

- Dogs: €25/month

- Cats: €24/month

AEDPAC notes this reflects greater formalization and adaptation to new regulatory expectations.

What This Means for the Pet Industry

- Spain is a high‑ownership, adoption‑driven market

- Spending is stable but more rationalized

- Physical retail remains dominant, unlike many EU markets

- Omnichannel behavior is now standard

- Health services and insurance are becoming more important

- Mixed feeding is rising, especially for cats

The Spanish market is evolving toward structured care, stable budgets, and strong retail loyalty.

Source:GlobalPETS