Jun 26, 2026Case Studies

$3.36 Billion in Quarterly Sales — But That's Not Why Chewy Leads the Pet Industry

Chewy generated $3.36B in Q1 sales and grew profit by 52%, yet still lowered its full‑year outlook.

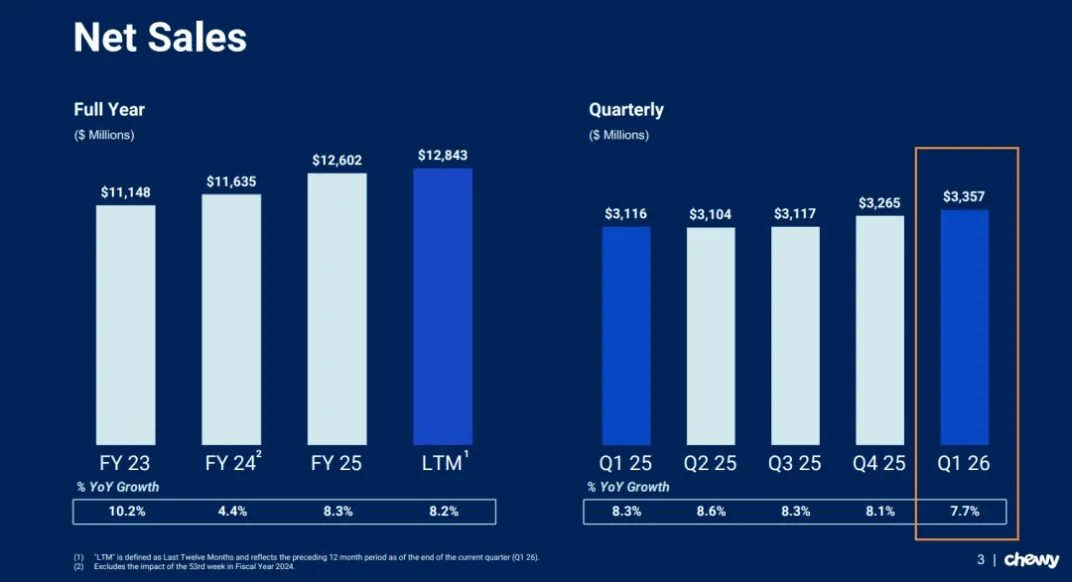

Chewy—the world’s largest online pet retailer—delivered another strong quarterly performance, generating $3.36 billion (¥22.72B RMB) in net sales during the first quarter of fiscal year 2026. Despite beating market expectations in both revenue and profit, the company surprised investors by lowering its full‑year outlook, signaling a strategic shift toward caution as the post‑pandemic pet spending boom cools.

Chewy’s Q1 results reveal a company that is not only maintaining scale but also strengthening profitability, operational efficiency, and long‑term strategic positioning. These factors explain why Chewy continues to be viewed as the global benchmark for pet e‑commerce.

1. Strong Sales, Even Stronger Profitability

Chewy’s Q1 net sales reached $3.36B, up 7.7% YoY, demonstrating stable demand despite a softer macro environment.

More importantly, profitability surged:

- Net income: $94.8M (+52% YoY)

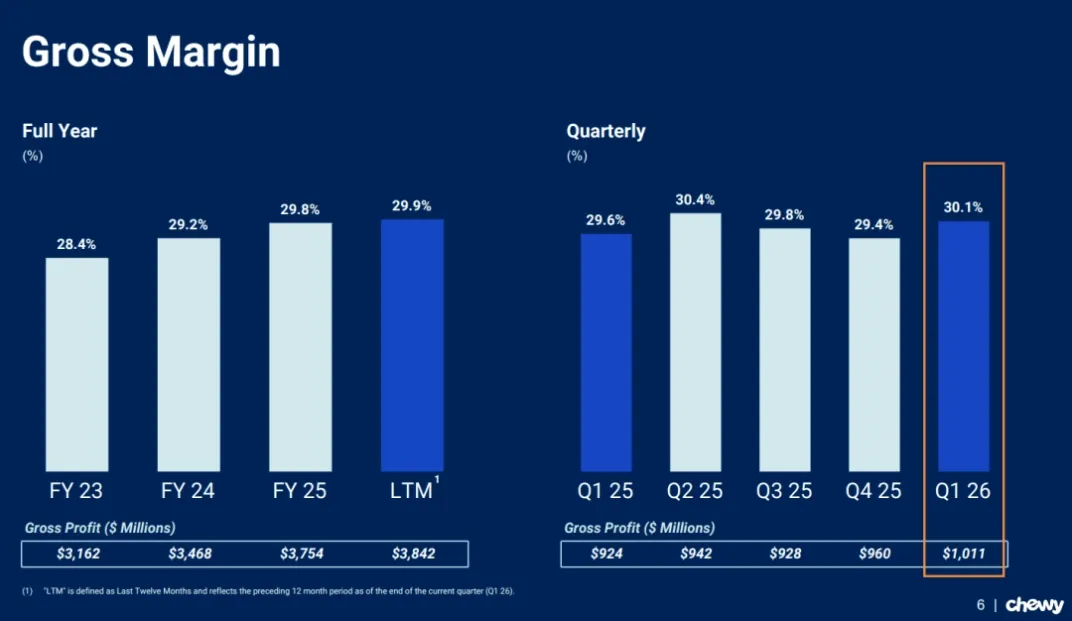

- Gross margin: 30.1% (+50 bps YoY)

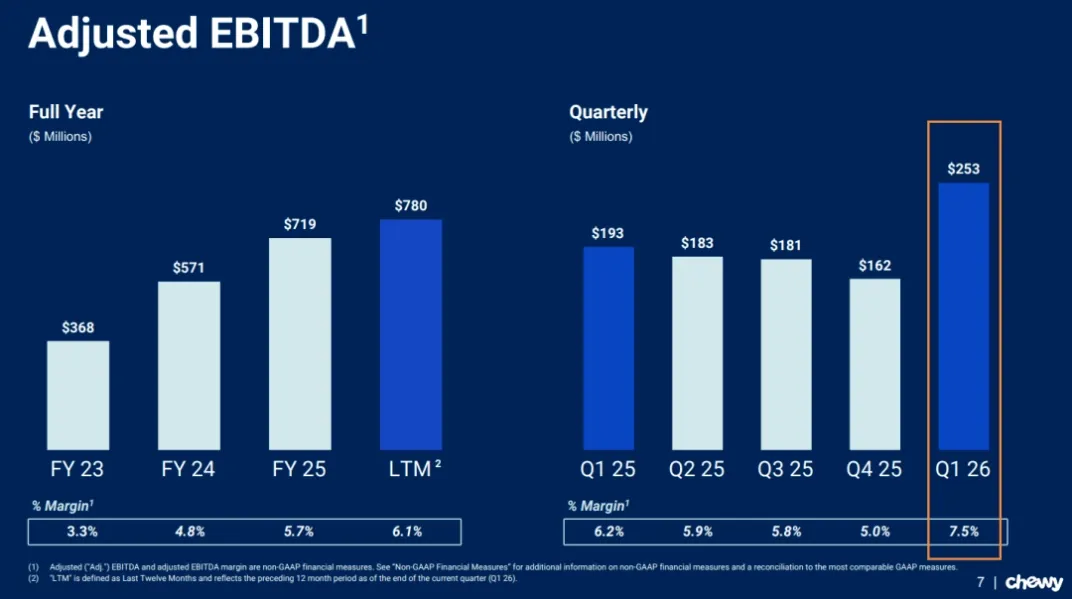

- Adjusted EBITDA: $253M (+$60.4M YoY)

- EBITDA margin: 7.5% (up from 6.2%)

CEO Sumit Singh attributes this performance to:

- Growth in sponsored ads

- A shift toward higher‑margin categories, especially health

- Automation and scale efficiencies reducing operating costs

These improvements reflect Chewy’s long‑term strategy paying off.

2. Autoship: The Engine Behind 84% of Revenue

One of Chewy’s most powerful advantages is its Autoship subscription model.

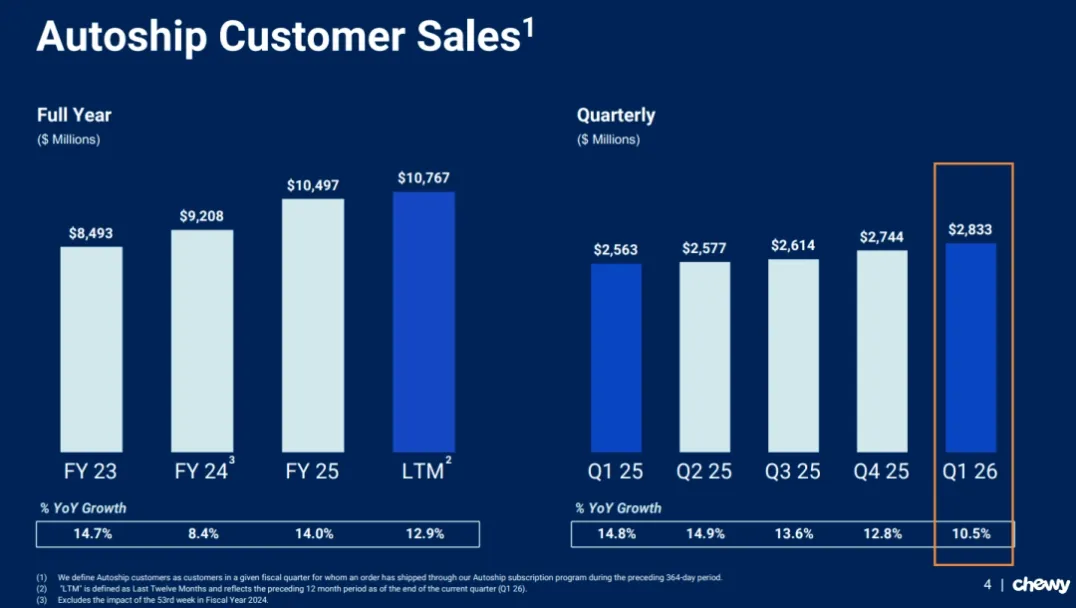

Q1 Autoship sales:

- $2.833B, up 10.5% YoY

- Represent 84.4% of total revenue

This means:

- Most orders require no human intervention

- Operational costs remain low

- Customer retention stays high

- Recurring revenue becomes predictable

High‑frequency consumables—like pet food and litter—fit perfectly into this model, and Chewy has optimized it better than any competitor.

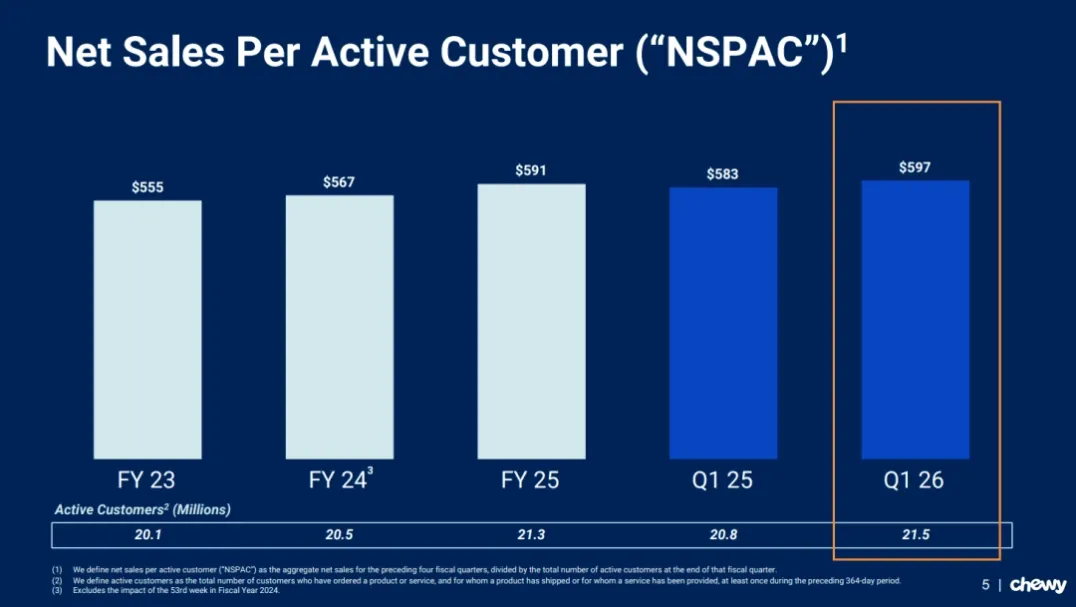

3. User Growth Slows, but Spending Per User Rises

Chewy’s active customers reached:

- 21.5 million, +3.6% YoY

- Net new customers: 170,000

While user growth has slowed, spending per user continues to rise:

- NSPAC (Net Sales Per Active Customer): $597, up from $583 YoY

This shows Chewy is shifting from acquisition to value expansion, extracting deeper lifetime value from existing customers.

4. Chewy’s Big Bet: Building a Veterinary Ecosystem

If selling pet food built Chewy’s foundation, veterinary services will define its future.

Modern Animal Acquisition

Chewy completed its acquisition of Modern Animal, adding:

- 29 new clinics

- Total clinics under Chewy Vet Care (CVC): 47

- Expected FY revenue contribution: $290M

By FY2026, Chewy expects to operate ~60 clinics, with 10–12 new openings planned.

SmartEquine Acquisition

Chewy also acquired SmartEquine from Covetrus:

- Expected FY contribution: $80M

Why This Matters

Veterinary care has:

- High trust barriers

- High margins

- Strong customer stickiness

And the results are already visible:

- 40% of CVC customers are new to Chewy

- These customers have an NSPAC of $900—far above platform average

Vet services are not just a new business—they are a high‑value customer acquisition engine.

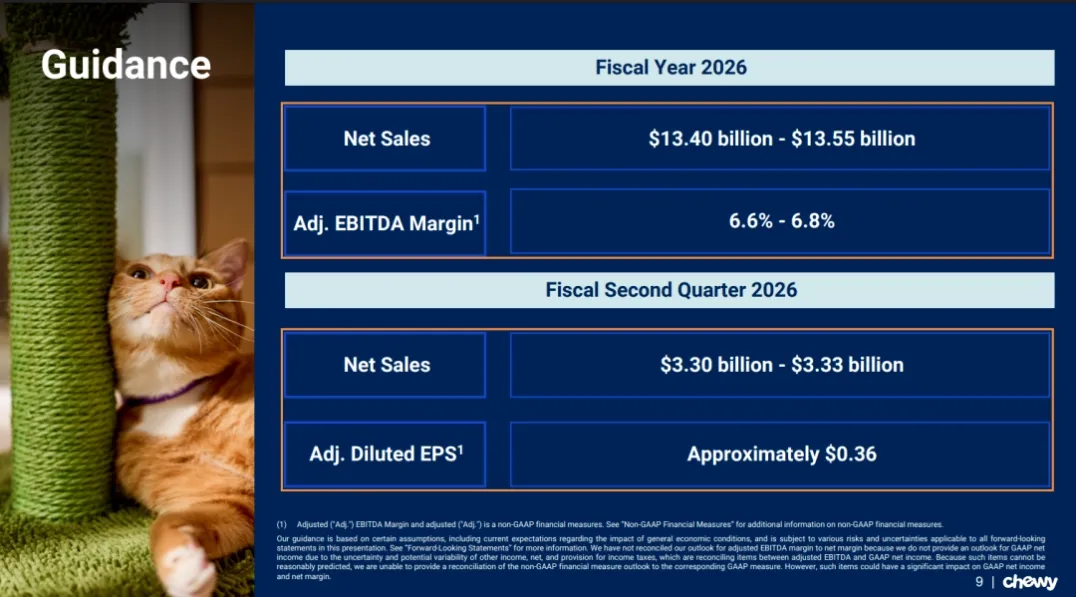

5. Why Lower Guidance Despite Strong Results?

Chewy revised its full‑year revenue forecast from:

- $13.6B–$13.8B → $13.4B–$13.6B

Q2 guidance was also lowered.

CEO Sumit Singh explained that the adjustment reflects a more conservative outlook due to:

- Inflationary pressure

- Weaker consumer confidence

- Slowing discretionary spending

This cautious stance is consistent with broader U.S. pet market trends, where growth has normalized after the pandemic boom.

6. Chewy’s Strategic Posture: Defend the Core, Expand the Future

Chewy’s Q1 performance shows a company balancing short‑term caution with long‑term ambition.

Defending the Core

- Strengthening Autoship

- Improving margins

- Expanding high‑frequency consumables

- Increasing operational automation

Expanding the Future

- Building a national veterinary ecosystem

- Integrating medical services with retail

- Enhancing customer lifetime value

- Creating a closed‑loop “care + commerce” model

Chewy is evolving from a retailer into a pet health ecosystem, which is why it remains the industry benchmark.

What This Means for the Pet Industry

- The era of explosive post‑pandemic growth is over

- Recurring revenue models (Autoship) are essential

- Veterinary services are becoming the next major battleground

- Profitability now matters more than scale

- Customer lifetime value is the new north star

Chewy’s strategy will influence how global pet brands, retailers, and OEM partners position themselves in the coming years.